Bank Recapitalisation

…what it is and what it means for the Nigerian economy.

In 2006, during the administration of Chief Soludo, the Nigerian banking sector experienced a significant recapitalisation that led to a massive reduction in the number of banks, case in point, from 89 banks to 24 banks. Now, nearly two decades later, the country faces a similar event.

First off, let’s get this big term out of the way. What is bank recapitalisation?

Every bank has capital and it comprises shares-ordinary and premium. This capital base shows the stability of the financial institution. Recapitalisation is the process where banks increase their capital base (long-term capital). In the Nigerian economy, the CBN is in charge of determining the capital base of these institutions.

Last year, during an annual banker’s dinner, Cardoso hinted at the need for recapitalization, emphasizing the necessity for financial institutions to be robust enough to support Nigeria's projected $1 trillion economy. Recapitalization would enhance banks' liquidity and strengthen their ability to lower medium to long-term lending rates. With increased capital, banks can absorb potential loan losses and withstand economic shocks more effectively. This financial stability enables them to offer lower interest rates, making borrowing more affordable for businesses and individuals. As a result, recapitalization not only strengthens the resilience of banks but also contributes to broader economic stability by facilitating access to credit and fostering growth opportunities.

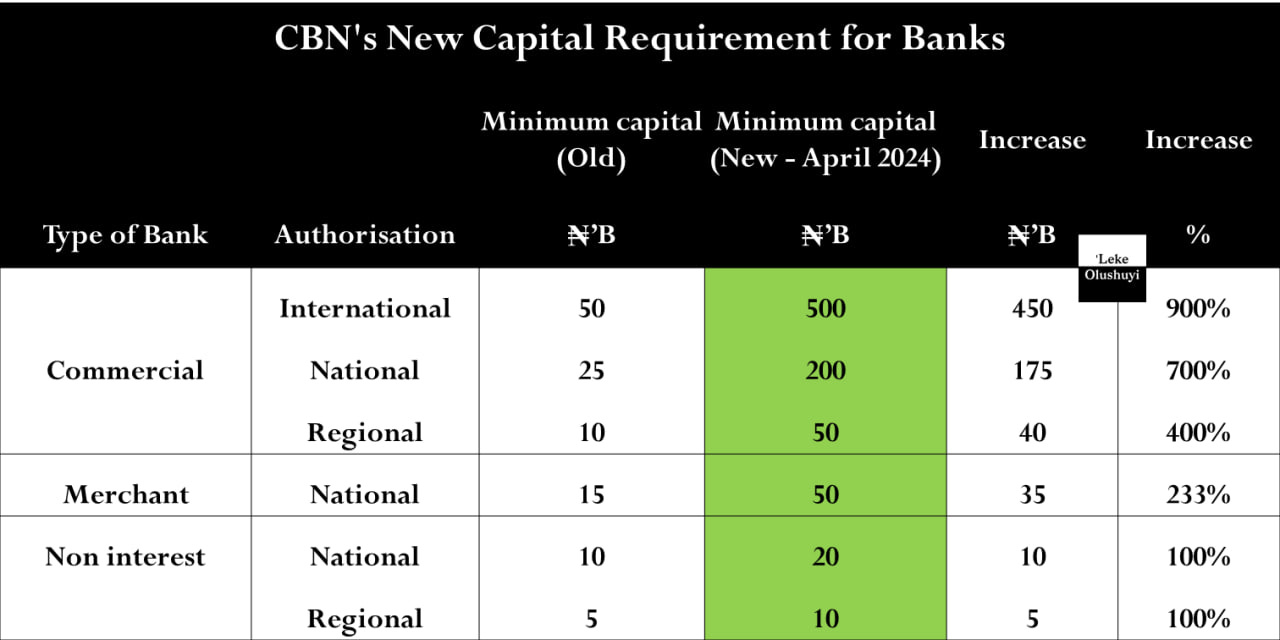

While the circular released on March 28th wasn't unexpected, the magnitude of the capital base increase came as a surprise. Each tier experienced more than a 100% increase, with tier 1 banks rising from 25 billion naira to 500 billion, and tier 2 banks from 25 billion naira to 200 billion naira. In contrast to the blanket increase in capital base mandated for all banks during Soludo's administration, this exercise allocated increases based on the categorization of banks. So what a merchant bank would be sourcing for would not be the same as what a commercial bank would be sourcing for.

The banks have been given two years to meet this target and a month to develop their strategy for acquiring more capital. Banks were presented with several options to fulfil the requirement: injecting fresh equity capital, engaging in mergers and acquisitions, or upgrading or downgrading their license status.

Possible reasons for recapitalisation include the depreciation of the naira. In 2006, 25 billion naira was about 250 million dollars. In 2024, 500 billion naira is approximately 358 million dollars ($1~N1308). Viewing from the lens of exchange rate, the increase in capital base is barely 50%. Additionally, there's talk of leveraging this process to attract foreign portfolio investment, as some banks may seek capital from investors outside Nigeria.

So What?

The adoption of the recapitalisation program was a well-thought-out plan. The CBN governor stated that stress tests showed that the economy's banks can fully handle this large task.

But it is important to note that although having a robust banking sector is crucial for economic stability it is overly simplistic to rely solely on banking reforms to solve Nigeria’s economic challenges. Enhancing the capital base of banks through recapitalisation is a positive step, but it is not a cure for all ills. The assumption that increased capital will automatically translate into more lending overlooks broader issues such as the overall business environment and macroeconomic factors.

Without a conducive environment for businesses to thrive, increased lending may not lead to desired economic growth. Addressing Nigeria's economic crisis requires a multifaceted approach that encompasses fiscal reforms, infrastructural development and improvements in sectors like education and agriculture. Moreover, investor confidence in the Nigerian business landscape is essential for sustainable growth.

In essence, while banking reforms are important, they are just one piece of the puzzle in achieving economic prosperity.

(Things are about to get interesting in the mergers and acquisition landscape)