New budget, same story

2023 proposed national budget

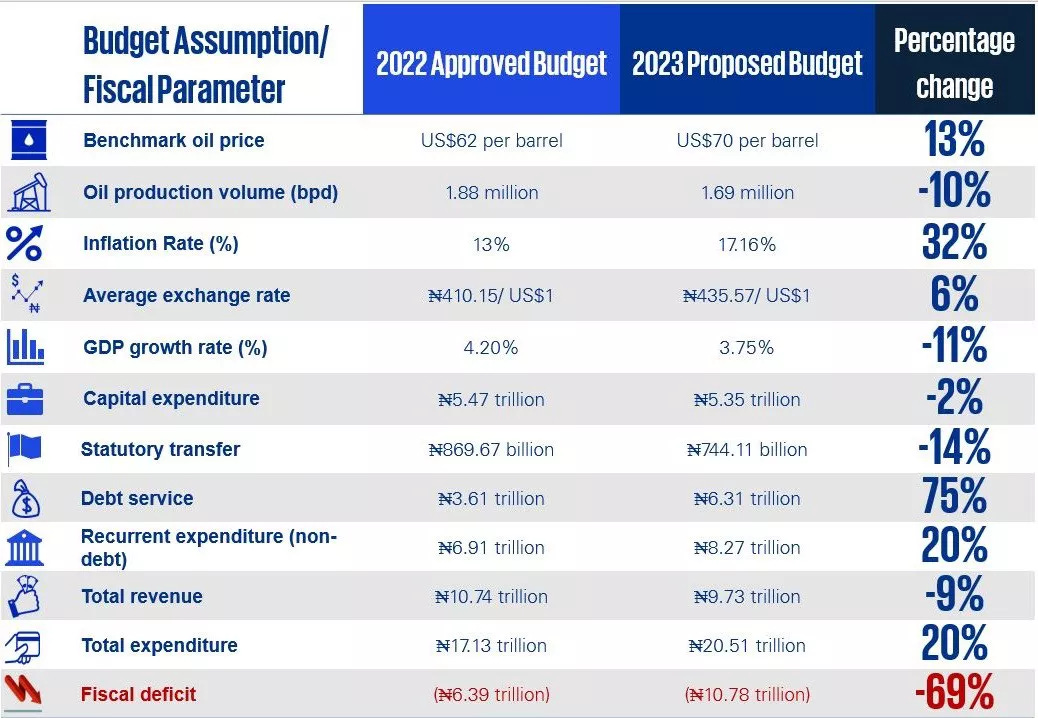

The Nigerian Federal Government recently proposed the 2023 national budget to the National Assembly for vetting and approval. The budget titled “Budget of Fiscal Sustainability and Transition” is the last of the current administration which has served the maximum of 2 terms (4 years each).

The budget has a proposed total revenue of 9.73 trillion Naira and expenditure 2.1x revenue at 20.5 trillion naira, a 10.7 trillion deficit. Key characteristics of the budget include a recurrent expenditure of 8.2 trillion naira, debt servicing at 6.3 trillion naira and the total allocation to capital expenditure stood at 5.3 trillion Naira.

The forecasts were based on some assumptions including oil price averaging 70 US dollars per barrel and the nation producing about 1.7 million barrels of oil per day in the coming year. If passed it will be Nigerians largest expenditure budget.

So What?

For a nation trying to propel economic growth, the increased size of the budget is welcome however looking at the breakdown of the budget, only 25 percent is dedicated to capital expenses and for reasons highlighted in our previous newsletter this is a continuation of a worrying trend. The deprioritization of capital investment affects the nations’ ability to grow and its ability to pay back loans.

Secondly, giving the issues currently plaguing the Nigerian oil industry with current production levels hovering around a million barrels a day, it remains to be seen how the government aims to achieve its production targets and with oil making up about 20 percent of the expected revenue (1.9 trillion naira) the achievement of this jump in production is critical to achieving the revenue targets.